| Issue |

BIO Web Conf.

Volume 68, 2023

44th World Congress of Vine and Wine

|

|

|---|---|---|

| Article Number | 03014 | |

| Number of page(s) | 7 | |

| Section | Law | |

| DOI | https://doi.org/10.1051/bioconf/20236803014 | |

| Published online | 23 November 2023 | |

Characteristics of dealcoholized and partially dealcoholized wines on company websites and their influence on the price

1 University of Foggia, Department of Humanities, via Arpi, 176, 71121 Foggia, Italy

2 University of Foggia, Department of Sciences of Agriculture, Food and Environment, via Napoli, 25, 71122 Foggia, Italy

Abstract

The market for beverages obtained from dealcoholization of wine has grown from $7.8 billion in 2018 to $10 billion in 2022 in ten key markets; IWSR forecasts that no- and low-alcohol products’ volume will grow by +8% yearly between 2022 and 2025. Considering the segment of non-alcoholic wine, its demand is expected to surge at a CAGR of 10% from 2023 to 2033 (2022 Report from Fact.MR). Companies have the opportunity to pursue product differentiation through the wide heterogeneity of attributes that can be communicated through the website. The purpose of this study is to examine the offerings of companies producing fully or partially dealcoholized wines, through the statistical analysis of data relating to the product attributes communicated by the websites. The data were collected considering a sample of 360 wines, fully or partially de-alcoholized, presented on 43 corporate websites, with reference to the following variables: company location, still/sparkling, color, grape origin, grape variety, container capacity, packaging material, alcohol content, alcohol removal technique, retail prices, awards/recognitions, certifications, production of conventional wines, production of other alcoholic beverages, places (virtual and physical) of purchase and presence on social media. The collected data fed into a database that was used to perform statistical analyses related to the variables considered, for each of which the relationship with product prices was considered.

© The Authors, published by EDP Sciences, 2023

This is an Open Access article distributed under the terms of the Creative Commons Attribution License 4.0, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article distributed under the terms of the Creative Commons Attribution License 4.0, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

1 Introduction

Consumer interest in moderate alcohol consumption has steadily grown over the past decade. Globally, self-moderation is on the rise, with over a third of regular wine consumers asserting that they have reduced their alcohol intake. This trend is particularly strong among younger demographics, specifically those from the so-called “Generation Z” and the “Millennials” [1]. Various factors drive this phenomenon: consumers are increasingly oriented towards a healthy lifestyle and proper diet, and public opinion has grown more sensitive to the controlled consumption of alcoholic beverages due to health recommendations and campaigns against alcohol abuse led by public institutions. This has led to greater awareness of responsible drinking.

Such a trend has spurred the development of non-alcoholic wines and low-alcohol wines. These beverages are made from grape must that has been fermented and subsequently dealcoholized, a process through which alcohol can be extracted from any alcoholic beverage. It is a delicate procedure requiring precise pressure and temperature conditions to prevent the loss of the wine's natural organoleptic properties.

The main consumers of dealcoholized and low-alcohol wines are those who abstain from or limit their intake of alcoholic beverages for various reasons: pregnant women, people undergoing therapeutic treatments or recovering from alcohol-related issues, professional drivers or people who need to drive at certain times, and consumers abstaining from alcohol due to dietary or religious reasons [2].

According to Wine Intelligence [1], a third of wine consumers in the USA are moderating their alcohol consumption. In Japan, 36% of consumers claim to self-moderate, compared to 58% in Switzerland and 56% in Australia. Italy, however, lags behind other countries. Germany and Spain boast the largest and most mature markets for non-alcoholic beverages, while the United Kingdom and the United States are among the most dynamic and are growing at a faster pace. Fact.MR website estimates that the US non-alcoholic wine market will see a Compound Annual Growth Rate (CAGR) of 9.6% during the period 2021-2031 [3].

The International Organization of Vine and Wine (OIV) has developed two resolutions as references: OIV-ECO 432-2012, “Beverage obtained from the dealcoholization of wine”, and OIV-ECO 433-2012, “Beverage obtained from the partial dealcoholization of wine” [4]. Such beverages can be obtained from wine or special wine and are subjected exclusively to specific treatments. Resolution OIV-OENO 394A-2012 defines the permitted dealcoholization techniques, including partial vacuum evaporation, membrane techniques, and distillation. The beverage obtained from the dealcoholization of wine may have an alcohol content by volume lower than 0.5% vol., while the beverage obtained from the partial dealcoholization of wine may have an alcoholic strength by volume equal to or greater than 0.5% vol. and lower than the minimum applicable alcoholic strength by volume of wine or special wine.

The aim of this study is to examine the offerings of companies producing wines that are fully or partially dealcoholized, through the analysis of product attributes communicated via the company's website.

2 The regulatory context

In the European Union, the regulation allowing the marketing of products under the legal name of “dealcoholized wine” or “partially dealcoholized wine” is the Regulation 2021/2117. This regulation amends EU Regulations 1308/2013 (single CMO), 1151/2012 (quality schemes for agricultural and food products), 251/2014 (definition, designation, presentation, labeling and protection of geographical indications of aromatized wine products) and 228/2013 (specific measures in the agriculture sector in favor of the outermost regions of the Union). The designation of the category of wine products may be accompanied by the term “dealcoholized” if the actual alcoholic strength of the product does not exceed 0.5% vol. It may be accompanied by the term “partially dealcoholized” if the actual alcoholic strength of the product is greater than 0.5% vol. and is lower than the minimum actual alcoholic strength of the category preceding the dealcoholization [5]. A limitation is foreseen for PDO and PGI wines, which cannot undergo total dealcoholization, but only partial. However, this partial dealcoholization must always be introduced following a modification of the relevant production regulations. Furthermore, the regulation, recalling the practices already allowed in the wine sector by the OIV Code for oenological treatments and incorporated in the EU Oenological Code, clarifies that dealcoholization processes are limited, alone or jointly, to partial vacuum evaporation, membrane techniques, and distillation.

Non-European countries regulate these products differently. In the United Kingdom, the 1996 “Food Labelling Regulations” define an “alcohol-free” beverage as one with an alcoholic content by volume not exceeding 0.05% [6]. The term “low alcohol” indicates a beverage with an alcoholic content not exceeding 1.2%. The term “dealcoholized” indicates a beverage obtained from an alcoholic beverage from which alcohol has been extracted, resulting in an alcoholic content by volume not exceeding 0.5%.

In the United States, wine falls under the regulation of the Federal Alcohol Administration Act (FAA Act), yet dealcoholized wines containing less than 7% Alcohol By Volume (ABV) are subject to the labeling provisions of federal law on food, drugs, and cosmetics, specifically the Federal Food, Drug, and Cosmetic Act. US federal law defines an alcoholic beverage as a product with an ethanol percentage equal to or greater than 0.5% ABV. Products containing less than 0.5% ABV can be defined as “non-alcoholic”, while the term “alcohol-free” can only be used when such products do not contain detectable alcohol [7].

As for alcoholic beverages sold in Canada, they are subject to various provisions:

- ■

Safe Food for Canadians Act (SFCA)

- ■

Safe Food for Canadians Regulations (SFCR)

- ■

Food and Drugs Act (FDA)

- ■

Food and Drug Regulations (FDR).

“Low alcohol” is an acceptable indication for a product with less than 1.1% ABV, while “Dealcoholized” means that the alcohol content has been reduced to less than 1.1% [8].

The Food Standards Australia New Zealand (FSANZ) is a statutory authority of the Australian government. Specifically, the Food Standards Code provides specific information requirements for labeling alcoholic beverages. According to the regulations, all beverages containing 0.5% or more alcohol must display information on the alcohol content on the label, and for alcoholic beverages containing more than 1.15% alcohol, the label must show the alcohol content as a percentage of ABV or milliliters/100 milliliters [9].

As for South America, with Decree 325/997, the “Reglamento Vitivinícola del Mercosur” came into effect, which sets the minimum alcohol content for wine at 7% (v/v at 20ºC) and also requires the label to display the definition “Vino parcialmente desalcoholizado” if the wine has undergone a process to reduce its alcohol content [10].

Finally, in South Africa, the “Liquor Products Act 60 of 1989” contains provisions that allow for the regulation of the production, labeling, import, and export of alcoholic products. In particular, “low alcohol” is defined as a wine with an alcohol content greater than 0.5% and less than 4.5%. On the other hand, “dealcoholized” can be defined as a wine with less than 0.5% alcohol, and finally, “alcohol-free” can be used if the alcohol content is less than 0.05% [11].

3 Scientific background

A review of the literature reveals that several studies have focused on the non-alcoholic wine market, some of which examine the analysis of consumer behavior and motivations behind the choice of these products. One reason consumers often avoid purchasing this type of wine is a perceived lack of taste. According to some research, “light” drinks are seen as “less tasty,” and this perception extends to alcoholic beverages as well [12]. On the contrary, an experimental study by Bucher et al. showed that consumers tend to consume the same amount of wine, whether it is a conventional or low-alcohol product [13].

According to Chrysochou, the growth of the low-alcohol beverage market is primarily due to numerous awareness campaigns against alcohol abuse [14]. Secondly, low-alcohol beverages are perceived as a way to reduce the negative health consequences caused by alcohol consumption. Therefore, these products align with the general trend of consumers leading a healthier lifestyle. A study by Meillon et al. also found that people tend to choose low-alcohol beverages because they are less caloric [15]. Pickering described how the improvement of dealcoholization technologies has led to an increase in wine quality [16]. Therefore, it is possible to produce low-alcohol wines that have highly acceptable sensory properties.

In the United Kingdom, according to a study conducted by Bruwer et al., the buyer profile mainly consists of women, Millennials, and Baby Boomers, with low-to-medium income who drink wine about once a week [17]. Furthermore, the study found that purchasing decisions are driven by a greater awareness of health issues related to the consumption of alcoholic beverages and the desire to buy low-cost wine. Accessibility seems to be another key factor as consumers claim that saving money is a reason to reduce alcohol consumption. From a specific study, it emerged that consumers tend to purchase dealcoholized wine only with a discount proportional to the reduction of alcohol content [18].

Finally, further investigations are needed to better understand how the perception and consumption of this type of wine change from one country to another and how much consumers are willing to pay. These considerations have influenced the choice of topic for this research, the objective of which was to understand how the different characteristics of dealcoholized wines are related to the selling price.Inizio modulo

4 Methodology

The methodology adopted to achieve the objective of this work consisted of the statistical analysis of data relating to the product attributes communicated by companies through the corporate website. The data were collected considering a sample of 360 wines, fully and partially de-alcoholized, presented on 43 corporate websites visited between September and October 2022. The data collection was carried out simulating the approach of the potential consumer who gathers information related to each product from the website with reference to the following variables: company location, type of still or sparkling wines, color, grape origin, grape variety, container capacity, packaging material, alcohol content, alcohol removal technique, retail prices, awards/recognitions, certifications, presence of conventional wines in the company portfolio, presence of other alcoholic beverages in the company portfolio, places (virtual and physical) of purchase, and presence on social media. The collected data fed into a database that was used to perform statistical analyses related to the variables considered, for each of which the relationship with product prices was considered.

5 Results and Discussion

Results obtained from the statistical analysis for each variable taken into consideration are described below.

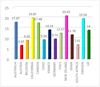

Figure 1 highlights that 21% of the considered companies are based in Germany, 16% in Spain, and 14% in Italy. Figure 2 shows the average wine prices distributed by Country. The highest average price, at 20.93 euros, is found among companies based in New Zealand, while the lowest average price of 6.65 euros is associated with companies based in Austria.

For 114 references, the origin of the grapes is not indicated on the website. As shown in Fig. 3, 25% of the wines are made from grapes produced in France, while 18% use grapes from Spain.

We also considered whether the references had received any acknowledgments. Of these, only 70 references had received an award, with an average price of 13.79 euros. In contrast, the average price for the 290 references without awards was 12.64 euros.

An analysis of the websites revealed that the product can carry either organic or Halal certification, the latter indicating compliance with Islamic doctrine during production (Table 1). In the sampled data, the majority of references, 67%, were to products without any certification, compared to a minority (33%) that were certified. Of the certified products, 12 percent carried only Halal certification, 16 percent were solely certified as ‘Organic’, and a mere 5 percent carried both certifications. Notably, it was observed that products bearing both certifications typically commanded higher average prices.

According to Table 2, 35% of the surveyed companies produce only dealcoholized or low-alcohol wine. In contrast, 33% manufacture not only dealcoholized wine, but also conventional wine and other alcoholic products. 23% produce both dealcoholized wine and other alcoholic beverages, and finally, 9% produce both dealcoholized and conventional wine. The highest average price is associated with wines produced by companies that manufacture both dealcoholized wine and other alcoholic products.

Concerning the color of the wines analyzed, 181 references were identified in the white wine category, 93 in red wines, and 86 in rosé wines. The average prices for ‘Red’ and ‘Rosé’ wines are similar, while ‘White’ wines have a slightly higher average price of 13.21 euros.

Furthermore, it was observed that 61% of the references fall into the ‘Still wine’ category, with the remaining 39% belonging to the ‘Sparkling wine’ category. The latter has a higher average price of 3.55 euros compared to the wines in the ‘Still’ category.

In the variable under consideration, the ‘Monovarietal’ category was found in 204 references, signifying that most of the wines are produced from grapes of a single variety (Table 3). However, 46 references belonged to the ‘Multivarietal with specified varieties’ category, indicating wines produced from different grape varieties that are specified on the website. Lastly, 11 references were produced from a blend of different, unspecified grape varieties, labeled as ‘Blend.’ As for average prices, they are similar for ‘Monovarietal’ and 'Missing Information' categories. The ‘Multivarietal with specified varieties’ records a higher average price (14.07 euros), meanwhile, the average price for 'Blend' appears to be the highest (15.91 euros). It's worth noting, though, that the number of references in this category is considerably lower than in the other categories, especially compared to ‘Monovarietal’ references.

As highlighted in Table 4, the majority of references have packaging with a capacity of 0.75 liters, which is indeed the most prevalent format. The average prices vary significantly, with the highest average price found for wines packaged in 0.20 liter containers. Glass packaging is used for almost all references, while aluminum packaging, although less common, commands the highest average price.

In the ‘Alcohol content’ variable (Table 5), ‘0%’ is the most common, accounting for 65% of the observations, followed by ‘<0.50%’ (25%). The differences in prices are significantly noticeable: we observe that references with an alcohol content of 0% and <0.50% have a higher average price than the others. On the other hand, wines with an alcohol content of 0.50% command the lowest average price.

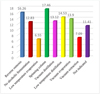

As can be seen from Fig. 4, in 33% of cases, the dealcoholization technique is not indicated on the website. Among the techniques disclosed on the company's website, the most prevalent is the spinning column, used in the production of 21% of the references, followed by vacuum distillation (17%), non-alcoholic fermentation (11%), and other techniques. When examining average prices, the differences are significant. Figure 5 shows that wines produced using the spinning column technique command higher prices, in contrast to wines produced through low-temperature evaporation, which have the lowest average price.

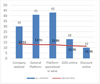

Figure 6 makes it clear that all companies retail their wines on specialized wine platforms, with almost all also selling through generalist platforms. Additionally, 70 percent of them sell through their corporate websites. However, sales through the websites of large-scale retail and discount stores are less prevalent. The highest average price is observed for products sold through company websites, while the lowest price is associated with wines sold on discount stores' websites, which isn't much lower than the price of wines sold through large-scale retail websites. Furthermore, it was noted that 54 percent of the wines cannot be purchased in a physical store but are exclusively available online. These wines command the highest average price, at 14.16 euros.

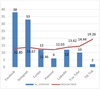

Finally, we observe how almost all companies have a presence on both Facebook and Instagram. The presence in the other socials turns out to be lower and differently distributed. The average price varies little between the different socials, however wines from the two companies using Tik Tok have the highest average price.

|

Figure 1 Distribution of companies by Country. |

|

Figure 2 Average price (€/liter) by Country. |

|

Figure 3 Grape origin indicated on the website. |

Certifications.

Conventional wine and other alcoholic products.

Variety.

Capacity.

Alcohol content.

|

Figure 4 Dealcoholization Technique. |

|

Figure 5 Average price (€/liter) for “Dealcoholization technique”. |

|

Figure 6 Online Distribution Channel. |

|

Figure 7 Social Media. |

6 Conclusion

The aim of this study is to examine the offerings of companies producing wines that are fully or partially dealcoholized, through the analysis of product attributes communicated via the company's website. The statistical analysis of data showed that the greatest number of companies producing non-alcoholic wine considered are located in Germany and Spain; these are indeed the largest and most mature markets for non-alcoholic beverages, in which the consumption of non-alcoholic wine is growing. However, the highest average price is found for wines produced by companies in New Zealand, California, and Sweden. The higher price in this case is likely due to the fact that there are still relatively few companies producing non-alcoholic wine in Sweden and New Zealand, so they can sell at a higher price in markets where there is demand for such products. Meanwhile, California, particularly Napa Valley, is a well-known area for conventional wine, which allows the companies to also attract attention for this new type of wines by selling them at a high price. Confirming this, it was found that the references produced with grapes from Napa Valley have the highest average price.

References that have both Halal and organic certifications have a higher average price; this is explained both by the higher production costs determined by the certification procedure and by the added value which corresponds to a willingness to pay on the part of the potential purchaser.

It was observed that 35% of the companies exclusively produce non-alcoholic wine and the highest average price was found for them; this is probably due to the fact that these companies, being specialized in the production of such products, have a wide range of offers that includes wines characterized by different price ranges.

Considering the typologies sill and sparkling, the highest average price was found for sparkling wines, and among the reasons for such result is that this type of product is considered “prestigious” and to be consumed on special occasions, involving also those people who cannot consume alcohol in participating to celebrations. It should also be considered that the production of sparkling wine has higher costs compared to still wine, which are reflected in the selling prices.

Furthermore, it was observed that most of the references are produced with a single variety of grape, however for them the average price is lower, while wines for which the different varieties of grapes used are not specified are more expensive.

From the analysis, it was possible to observe that the 0.75 liter format and glass packaging prevail; cans and bottles with a smaller capacity are less widespread because they have a higher purchase cost for the company and also because as the quantity purchased by the customer increases, the company offers discounts that result in a reduction of the unit price.

Most of the considered wines have an alcohol content equal to 0% and the most frequent dealcoholization technique was found to be the spinning column. The lower average price was found for the dealcoholization technique consisting of low-temperature evaporation, which was found to be the least expensive as opposed to the spinning column technique which is the most expensive.

As far as distribution channels are concerned, all companies sell their products through platforms specializing in wine but the highest average price is found for products sold through the company's website; this could be due to the different costs of logistics, shipping and packaging, which the company has to bear to ship its products to customers distributed around the world. On the contrary, for wines purchasable at a physical store and through the websites of large-scale retail and discount, a lower average price was observed; this reason of that could be that often physical sales points and discounts implement price strategies that provide discounts depending on the periods and the location of the shop. In addition, larger companies can take advantage of economies of scale and therefore sell high volumes of product at a lower price.

Finally, it was observed that all companies are present on the main social media and in particular, almost all of them are present on Facebook; social media is indeed a very important channel to make their products known and purchased.

In conclusion, the data shows that in some countries the non-alcoholic wine market is already developed and continuously growing while in countries characterized by a low diffusion of such products, companies should analyze the market and devise suitable strategies to best enhance their product.

References

- https://www.wineintelligence.com/ [Google Scholar]

- https://www.winemonitor.it/ [Google Scholar]

- https://www.factmr.com/report/4532/non-alcoholic-wine-market [Google Scholar]

- https://www.oiv.int/it [Google Scholar]

- https://www.politicheagricole.it/flex/cm/pages/ServeBLOB.php/L/IT/IDPagina/17582 [Google Scholar]

- https://www.food.gov.uk/business-guidance/wine-labelling [Google Scholar]

- https://www.fda.gov/regulatory-information/search-fda-guidance-documents/cpg-sec-510400-dealcoholized-wine-and-malt-beverages-labeling [Google Scholar]

- https://inspection.canada.ca/eng/1297964599443/1297965645317 [Google Scholar]

- https://www.foodstandards.gov.au/Pages/default.aspx [Google Scholar]

- https://www.argentina.gob.ar/sites/default/files/reglamentovitivinicoladel_mercosur.pdf [Google Scholar]

- https://www.gov.za/documents/liquor-products-act-24-mar-2015-1450 [Google Scholar]

- Porretta, S., Donadini, G. A preference study for no alcohol beer in Italy using quantitative concept analysis. J. Inst. Brew. 114, 315–321, 2008 [CrossRef] [Google Scholar]

- Bucher, T., Frey, E., Wilczynska, M., Deroover, K., Dohle, S. Consumer perception and behaviour related to low-alcohol wine: Do people overcompensate? Public Health Nutr. 23, 1939–1947 (2020) [CrossRef] [PubMed] [Google Scholar]

- Chrysochou, P. Drink to get drunk or stay healthy? Exploring consumers’ perceptions, motives and preferences for light beer. Food Qual. Prefer. 31, 156–163 (2010) [Google Scholar]

- Meillon, S., Dugas, V., Urbano, C., & Schlich, P.. Preference and acceptability of partially dealcoholized white and red wines by consumers and professionals. American journal of enology and viticulture 61(1), 42–52 (2010) [CrossRef] [Google Scholar]

- Pickering, G.J. Low-and reduced-alcohol wine: A review. J. Wine Res. 11, 129–144 (2000) [CrossRef] [Google Scholar]

- Bruwer, J., Jiranek, V., Halstead, L., & Saliba, A. Lower alcohol wines in the UK market: some baseline consumer behaviour metrics. British Food Journal (2014) [Google Scholar]

- Stasi, A., Bimbo, F., Viscecchia, R., & Seccia, A. Italian consumers ׳preferences regarding dealcoholized wine, information and price. Wine Economics and Policy 3(1), 54–61 (2014) [CrossRef] [Google Scholar]

All Tables

All Figures

|

Figure 1 Distribution of companies by Country. |

| In the text | |

|

Figure 2 Average price (€/liter) by Country. |

| In the text | |

|

Figure 3 Grape origin indicated on the website. |

| In the text | |

|

Figure 4 Dealcoholization Technique. |

| In the text | |

|

Figure 5 Average price (€/liter) for “Dealcoholization technique”. |

| In the text | |

|

Figure 6 Online Distribution Channel. |

| In the text | |

|

Figure 7 Social Media. |

| In the text | |

Current usage metrics show cumulative count of Article Views (full-text article views including HTML views, PDF and ePub downloads, according to the available data) and Abstracts Views on Vision4Press platform.

Data correspond to usage on the plateform after 2015. The current usage metrics is available 48-96 hours after online publication and is updated daily on week days.

Initial download of the metrics may take a while.