| Issue |

BIO Web Conf.

Volume 17, 2020

International Scientific-Practical Conference “Agriculture and Food Security: Technology, Innovation, Markets, Human Resources” (FIES 2019)

|

|

|---|---|---|

| Article Number | 00003 | |

| Number of page(s) | 6 | |

| DOI | https://doi.org/10.1051/bioconf/20201700003 | |

| Published online | 28 February 2020 | |

Comparative analysis of plant growth risks insurance in the Eurasian Economic Union countries

1

Belarusian State Economic University, Minsk, 220070, The Republic of Belarus

2

Samara State Agrarian Unversity, Kinel, 446442, Russia

3

S. Seifullin Kazakh Agrotechnical University, Nur-Sultan, 010011, The Republic of Kazakhstan

* Corresponding author: This email address is being protected from spambots. You need JavaScript enabled to view it.

Abstract

The article presents the results of a comparative analysis of the procedure for conducting compulsory insurance of crops in three states of the Eurasian Economic Union – the Russian Federation, the Republic of Belarus and the Republic of Kazakhstan. The authors analyzed the main conditions for its implementation, the differences in the regulatory framework for the provision of state support, the dynamics of key indicators of development of this type of insurance, revealed the reasons for their changes. The ways of improving the state support for crop insurance in the EAEU countries are proposed.

© The Authors, published by EDP Sciences, 2020

This is an Open Access article distributed under the terms of the Creative Commons Attribution License 4.0, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article distributed under the terms of the Creative Commons Attribution License 4.0, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

1 Introduction

Agricultural production is the most vulnerable area of business. Its implementation carries significant risks. The output of ready agricultural products is influenced not only by the volume of financial investments and labor costs, but also by constant changes in natural and climatic conditions, seasonality of production, man-made disasters, a long cycle of ripening and storage of agricultural crops, etc. In this regard, conscious risk management is important for the implementation of the main tasks of enterprises of the agro-industrial complex [1–3]. As many scientists note, risk management includes an assessment of its degree, the process of implementing specific events that help minimize the negative impact of external and internal factors of the external and internal environment, bringing different losses [4–6]. In this case, the importance of not only an accurate assessment of the degree of risk increases, but also the search for minimizing its negative consequences. The most traditional methods of covering risk losses in the past and present time include insurance of the process of growing crops, which is one of the effective mechanisms for financial protection of agricultural producers [7–10]. The growth of insurance operations is expected in Eurasian Economic Union Countries (hereinafter – EAEUC) that could reduce the risk in agriculture, thereby reducing the negative consequences of the occurrence of adverse natural events as well as price fluctuations in the market.

2 Materials and methods

At present, the single agricultural insurance market of EAEU countries has just started to grow. Its development is negatively affected by the high cost of insurance services associated with the presence of significant risks in agriculture as well as the insufficiently active policy of promoting these operations by insurance companies and EAEU member states, relatively low level of information base of agricultural producers.

A project for the formation of a single insurance market is being developed by the decision of the Eurasian Congress of insurance companies across Eurasian Economic Union countries. To achieve this goal, organizational, managerial and economic prerequisites must be established: the harmonization of national legislation has been gradually completed and the basic requirements for insurance companies have been defined.

541 insurance companies operated across EAEU countries in 2012. Their number significantly had declined by 1.01.2018 and comprised just over 300 policy holders [11]. They offer personal and property insurance, liability insurance and a range of special insurance services. (Table 1).

The integration of insurance markets began in 2005 from the establishment of Interstate Coordination Council of Heads of Insurance Supervision States – CIS participants, by the decision of which the costs incurred in the production of crop products must be insured without fail. However, the mechanism of providing State Support across CIS countries has been different and defined in separate periods of time. In Russia, the insurance premium in the amount of 50% is reimbursed from the state budget, 95% in Belarus, and in Kazakhstan the state compensates insurance companies for the paid insurance indemnities in the amount of 50%. There are other conditions for this type of insurance.

Number of Insurance Companies in EAEUC, 2012–2017, units

3 Results and discussion

In the Russian Federation, since 1991, agricultural insurance in crop production with the state participation is voluntary. In accordance with the Law of the RSFSR “On the social development of a village” for Soviet farms, collective farms, farmers, peasant (farmer) farms and other agricultural enterprises of Russia, compulsory agricultural insurance was replaced by voluntary including sowing crops, trees (bushes), fruit and berries and other long-term trees and shrubs [12].

Crop insurance was sporadic due to the severe turbulence of the economic situation before 2003, in the framework of which, due to unfavorable pricing conditions, farmers were forced to finance technological issues immediately. Active promotion of agricultural insurance by means of state support commenced in 2003. Initial conditions were very favorable.

For example, across Samara Region in 2003–2006, as part of crop insurance by means of State Support from the Federal Budget, 50% was compensated from insurance premiums, 30% – from Regional Budget and 20% was paid by an agricultural enterprise. The terms and conditions have been changed since 2007 – consolidated budget compensated just 50% of the premium. The following change of the form of the state participation in crop insurance refers to 2011, Federal Law № 260-FL «Upon the State Support in the field of agricultural insurance and amendments in the Federal Law «Upon the development of Agriculture» was adopted. In it, in particular, the form of subsidies was changed. If before that, the agricultural company paid 100% of the insurance premium at the time of entering into the insurance contract and only subsequently received appropriate compensation from the state budget, now, in accordance with Paragraph 3. Art. 3 of this Law – the subsidy is transferred “... to the insurer’s current account in the amount of 50% of the accrued insurance premium on the basis of the application of an agricultural producer”.

Additionally, a policyholder was enabled to approach more flexibly to the formation of the insurance premium amount due to the use of the unconditional franchise in the range from 0 to 30% (previously, its value was fixed at 20%) [12].

As a result of changes in approaches to the state support, significant fluctuations in insurance results can be noted in the Russian Federation (Table 2).

As can be seen from Table 2, the state-backed insurance market has actively responded to changes in legislation, which was accompanied by an increase in the number of contracts concluded and the amount of insurance premium.

However, a long period with relatively favorable climatic conditions, and as a result, a low ratio of reimbursement and funds spent led to a massive rejection of the use of crop insurance by means of the state support. If 18.5% of all the acreage of Russia was insured in 2012, it comprised only 5.0% in 2016. At the same time, a wider spread of crop insurance without the state support can be noted. At a lower cost for a policyholder (in 2016, in accordance with «Federal Agency of the State Support AIC (AgroIndustrial Complex)», the average tariff accounted for 1.2% against 5.47% by means of the state support, and the level of payments – 262.7%) [12].

These data indicate that the crop insurance method by means of the state support, both in determining insurance tariffs, and in optimizing the determination of the parameters of the insurance system requires further improvement.

In Belarus, on compulsory insurance by means of the state support for the crop harvests, livestock and poultry (hereinafter – CISSCHLP), a policyholder himself/herself pays only 5% of the insurance premium, and 95% is financed from the state budget. The only policyholder for this type of insurance is the state Company Belgosstrakh, which accumulates half of the insurance premiums in the Belarusian insurance market.Each year, the Decree of the President of the Republic of Belarus determines the crops that are subject to compulsory insurance and the percentage of compensatory damages. Information about these conditions are presented in Table 3.

As can be seen from Table 3, the list of crops insured and the percentage of compensatory damages for 11 years of operation of CISSCHLP constantly changed and by 2017 had reduced up to two crops (winter rape and flax fiber). The percentage of the compensatory damage sharply dropped (up to 17%).

Insurance rates are also high upon CISSHCLP. They differ in different regions of the Republic of Belarus, since they take into account their different climatic conditions and statistics of occurrence of insured events in previous years (Table 4).

Insurance rates upon the insurance of crops have been significantly increased compared to the previous 2018 and established in 2019 upon winter rape in the range between 6 and 25% (from 4 up to 17% in 2018) and flax fiber – from 0.7 up to 4.02% (from 0.5 up to 2.5%).

Such high rates for agricultural producers would be hard to pay without the State Support in the form of 95 per cent coverage from the State Budget of the the Republic of Belarus.

However, they also do not allow Belgosstrakh to carry out this type of insurance profitably in all years. The leveling of risks in this segment often occurs at the expense of other insurance products, since the accumulated special insurance reserve for this type of insurance is almost completely used.

Therefore, the insurance coverage over the past 10 years has decreased significantly. One of the reasons is the high unprofitability of this compulsory type of insurance (Table 5).

The dynamics of insurance premiums for 2008–2018 differs from the uneven growth of their income. 95% of them comprised the budget resources and only 5% was paid by agricultural companies. Mobilized insurance premiums were used to cover unexpected crop losses, including reseeding.

The volume of payments for seperate years depended on the actual size of the damage to the Republic’s agriculture. In 2018, winter rape crops were again affected by freezing, and flax fibre by a spring drought. Insurance payments for the first half of 2018 were closer to the received contributions.

However, some restoration of the insurance reserve on the results of 2017 allowed one to plan an increase in the percentage of compensatory damages from 17% to 30% in 2019.

Thus, in the Republic of Belarus, the state annually applies compulsory insurance to cover damage to agriculture and ensures its development to meet the food needs of the population of the Republic.

In Kazakhstan, compulsory crop insurance was introduced in 2004. Over the years of the insurance program, no fundamental changes have occurred, except for granting the right to insure their risks to agricultural producers by uniting into mutual insurance societies (hereinafter – MIS).

Initially, in 2004, 7 insurance companies dealt with agricultural insurance (hereinafter – IC).

However, due to the significant risk and, consequently, the unprofitability of this type of insurance, currently, in the compulsory insurance market of crops in Kazakhstan, there are just only two IC: established by the state in 1995 JSC «Daughter Insurance Company of the People’s Bank of Kazakhstan «Khalyk-Kazinstrakh» and JSC “Grain Insurance Company” established in 2003 and specialized in providing insurance protection for agricultural companies.

They provide not only insurance in the field of crop production, but also many other types of insurance, which cover losses incurred in crop insurance. The work of the MIS is different in that the next insurance premiums can be reduced by the general meeting of the company’s members, if at the end of the accounting period the company had no arrears in insurance payments, taxes and other obligatory payments to the budget. The crop areas insured by them for 2014–2017 are presented in Figure 1.

The area of insured MIS crops during the analyzed period decreased significantly. If 3.9 million hectares (33%) were insured in 2014, then just 0.7 million hectares (6.2%) were insured in 2017. Then IC extended insured fields from 7.8 million hectares in 2014 up to 11.0 million hectares in 2017.

The Law of the Republic of Kazakhstan “On Insurance” establishes minimum and maximum rates for groups of cultures. The size of insurance rates for compulsory insurance in the crop industry of Kazakhstan are differentiated by types of crops and by regions (Table 6).

As a rule, in practice, the amount of insurance premiums due to the low solvency of agricultural producers is calculated at the minimum insurance rate. This does not allow to form a sufficient reserve for insurance payments, which adversely affects the financial stability of insurance companies, especially when insurance events occur.

Another problem in Kazakhstan is the lack of readiness of insurance companies to organize insurance properly in the agricultural sector. Representatives of policy holders do not have time to inspect crops on time, assess the size of losses, and mobilize resources for their compensation.

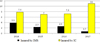

In recent years, insurance companies have suffered significant financial losses in compulsory insurance of crops and therefore give up their business. The main indicators of insurance companies of Kazakhstan on compulsory insurance of crop production are presented in Figure 2.

As can be seen, the value of mobilized insurance premiums in Kazakhstan over the past 10 years has fluctuated smoothly and almost doubled by 2018 compared to 2009. As for insurance payments, in certain years, the payments significantly exceeded the premiums accumulated for this type of insurance. This was due to severe drought in the Republic in 2008, 2010, 2012 and 2014 which led to the the loss of crops and, accordingly, to the spasmodic growth of insurance payments.

In more favorable 2015–2018 years insurance premiums exceeded payouts. The average loss ratio for this type of insurance for the analised period comprised 89%, however, a measure of the spread of data around the average value reflects a significant variance in a number of payments, the standard deviation comprised 419 mln tenge.

The State Support of compulsory insurance in crop production in the Republic of Kazakhstan in the analyzed period was carried out by allocating budget funds to the authorized state body in the field of crop production for reimbursement of 50% of insurance payments to IC and MIS for insured events resulting from adverse natural phenomena, as well as to pay for agent services.

The analysis of the national insurance market of Kazakhstan allows us to conclude that crop insurance occupies an insignificant place in the total volume of compulsory insurance: from 1 to 1.7% until 2013, and in the last four years of the analyzed period, its share decreased even more in 2017 accounted for only 0.3% of the total income of the insurance sector in Kazakhstan. These indicators imply the drawbacks in the organization of this type of insurance, which affects the weakness of the financial protection of the industry.

Insured Agricultural crops and the percentage of compensatory damages under CISSCHLP in the Republic of Belarus, 2008–2019

|

Fig. 2. The main indicators of insurance of crop production in Kazakhstan, 2008–2018 (mln tenge) |

4 Conclusion

Meanwhile, as the world practice confirms, insurance acquires paramount importance in enhancing the financial protection of agricultural producers, which is subject to significant losses due to the influence of anomalous natural and climatic conditions. These problems are sharpened by the integration of many countries into EAEU, uniting a large population. They need to expand the food program, largely dependent on the state of their agriculture in the common territory of the community.

One of the active tools of its development can be compulsory and voluntary insurance of crop harvests, mitigating the inevitable losses from natural and climatic phenomena.

The solution to this problem is complicated not only by significant natural differences of the member – states of EAEU, but a differentiated level of a comapny and state of agricultural insurance in different countries, as well as the degree of economic development and other national characteristics. In this regard, at the initial stage of the formation of a single insurance market for EAEU, the unification of the rules of operation of the single insurance market as well as the method of calculating its key indicators, becomes possible only after the proper development of national insurance markets and their convergence, facilitation of modernization and enhancement of the financial protection of all sectors of the economy and population from unforeseen losses. As one of the important insurance objects that are actively influencing the reduction of the riskiness of agriculture and its development, insurance of crop harvests should be compulsory and voluntary.

Acknowlegement

This article was prepared with the support of the Belarusian Republican Foundation for Fundamental Research.

References

- J. Yu, D.A. Sumner, Agricultural Economics (United Kingdom) 49(4), 533–545 (2018) [CrossRef] [Google Scholar]

- S. Shaik, K.H. Coble, T.O. Knight, A.E. Baquet, G.F. Patrick, J. Agr. Appl. Econ. 40(3), 757–766 (2008) [CrossRef] [Google Scholar]

- V.H. Smith, J.W. Glauber, Applied Economic Perspectives and Policy 34(3), 363–390 (2012) [Google Scholar]

- T.A. Verezubova, T.V. Sorokina, Insurance in the system of financial services in Russia: place, issues, transformation 1, 259–263 (Kostroma State University, Kostroma, 2017) (In Russ.) [Google Scholar]

- N.V. Kirienko, I.A. Kazakevich, Bulletin of the Belarus State Economic University 3, 86–93 (2014) (In Russ.) [Google Scholar]

- B.J. Barnett, J.R. Black, Y. Hu, J.R. Skees, J. of Agricultural and Resource Economics 30(2), 285–301 (2005) [Google Scholar]

- K.H. Coble, B.J. Barnett, American J. of Agricultural Economics 95(2), 498–504 (2013) [CrossRef] [Google Scholar]

- C. Rosenzweig, J. Elliott, D. Deryng, A.C. Ruane, C. Muller, A. Arneth, K.J. Boote, J.W. Jones, Proc. of the National Academy of Sciences of the United States of America 111(9), 3268–3273 (2014) [CrossRef] [Google Scholar]

- M.J. Roberts, W. Schlenker, J. Eyer, American J. of Agricultural Economics 95(2), 236–243 (2013) [CrossRef] [Google Scholar]

- R.M. Rejesus, K.H. Coble, M.F. Miller, R. Boyles, B.K. Goodwin, T.O. Knight, J. of Agricultural and Resource Economics 40(2), 306–324 (2015) [Google Scholar]

- Financial Organizations in Eurasian Economic Union. 2013–2017 Retrieved from: http://eec.eaeunion.org/ru/act/integr_i_makroec/dep _stat/fin_stat/statistical_publications/Documents/fin stat_3/finstat_3_2017.pdf (In Russ.) [Google Scholar]

- T.A. Verezubova, K.A. Zhichkin, A.M. Mukhitbekova, Finance 10, 55–60 (2018) (In Russ.) [Google Scholar]

- Central Bank of the Russian Federation Retrieved from: http://www.cbr.ru (In Russ.) [Google Scholar]

- Report upon the state of the agricultural insurance market, executed by means of State Support in the Russian Federation in 2016 Retrieved from: http://fagps.ru/getfile/d5f79a4a5357e4665ef6a5cb1d 543295/9.pdf (In Russ.) [Google Scholar]

- Belgosstrakh Retrieved from: http://www.bgs.by (In Russ.) [Google Scholar]

- National Bank of Kazakhstan Retrieved from: http://www.nationalbank.kz. (In Russ.) [Google Scholar]

- B. Aimurzina, M. Kamenova, A. Omarova, A. Karipova, A. Khoich, J. of Environmental Management and Tourism 9(6), 1342–1350 (2018) [CrossRef] [Google Scholar]

All Tables

Insured Agricultural crops and the percentage of compensatory damages under CISSCHLP in the Republic of Belarus, 2008–2019

All Figures

|

Fig. 1. Dynamics of insured crops in Kazakhstan for 2014 – 2017, million hectares [16] |

| In the text | |

|

Fig. 2. The main indicators of insurance of crop production in Kazakhstan, 2008–2018 (mln tenge) |

| In the text | |

Current usage metrics show cumulative count of Article Views (full-text article views including HTML views, PDF and ePub downloads, according to the available data) and Abstracts Views on Vision4Press platform.

Data correspond to usage on the plateform after 2015. The current usage metrics is available 48-96 hours after online publication and is updated daily on week days.

Initial download of the metrics may take a while.